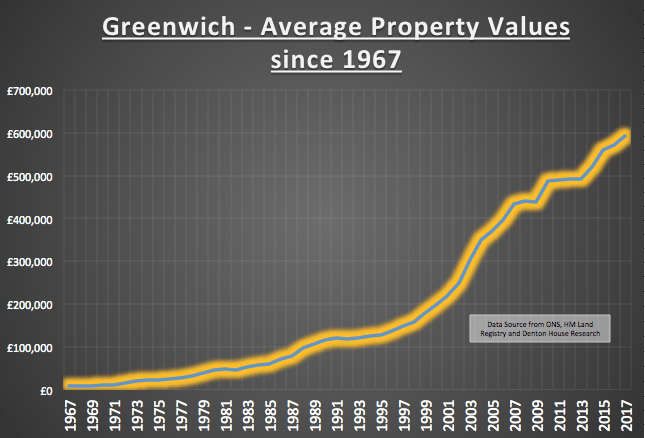

“What’s happening to the Greenwich Property Market” is a question I am asked repeatedly. Well, would it be a surprise to hear that my own research suggests that there isn’t just one big Greenwich property market – but many small micro-property markets?

According to recent data released by the Office of National Statistics (ONS), I have discovered that at least three of these micro-property markets have emerged over the last 20+ years in the borough.

For ease, I have named them the …

- ‘lower’ Greenwich Property Market.

- ‘lower to middle’ Greenwich Property Market.

- ‘middle’ Greenwich Property Market.

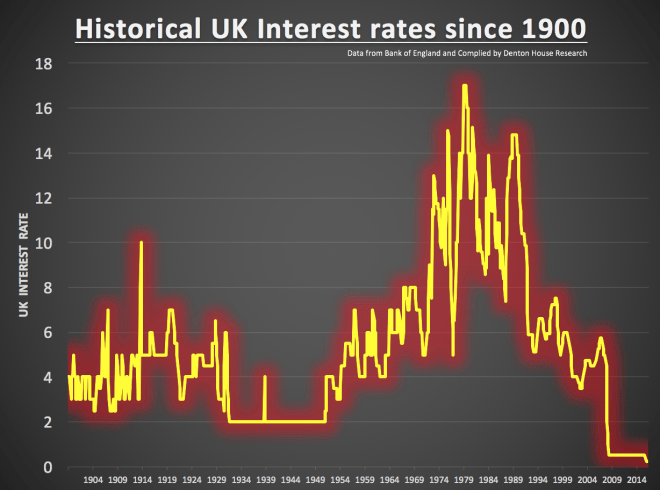

The ‘lower’ and ‘lower to middle’ sectors of the Greenwich property market have been fuelled over the last few years by two sets of buyers. The first set, making up the clear majority of those buyers, are cash rich landlord investors who are throwing themselves into the Greenwich property market to take advantage of alluringly low prices and even lower interest rates. The other set of buyers in the ‘lower’ and ‘lower to middle’ Greenwich property market are the first-time buyers (FTB), although the FTB market is in a state of unparalleled deadlock as it’s been trampled into near-immobility and incapacity by the new 2014 stricter mortgage affordability regulations and also fewer mortgages with low deposits.

Some of you may be interested to know how I have classified the three sectors ..

- ‘lower’ Greenwich housing market – the bottom 10% (in terms of value) of properties sold

- ‘lower to middle’ Greenwich housing market – lower Quartile (or lowest 25% in terms of value) of properties sold

- ‘middle’ Greenwich housing market – which is the median in terms of value

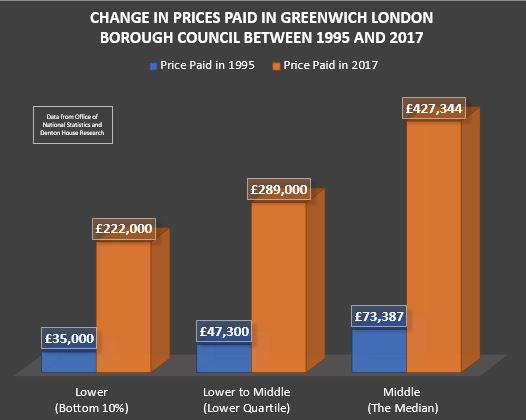

…. and if one looks at the figures for Greenwich London Borough Council area you can see the three different sectors (lower, lower/middle and middle) have performed quite differently.

|

Greenwich London Borough Council Property Market – Sold Prices |

Price Paid in 1995 | Price Paid in 2017 | Percentage Uplift 1995 – 2017 |

|

Lower (Bottom 10%) |

£35,000 | £222,000 | 534.29% |

|

Lower to Middle (Lower Quartile) |

£47,300 |

£289,000 | 510.99% |

|

Middle (The Median) |

£73,387 | £427,344 |

482.31% |

You can quite clearly see that it is the ‘lower” market that has performed the best.

You might ask, what do all these different figures mean to homeowners and landlords alike? Quite a lot – so let me explain. The worst performing sector (with the lowest Percentage uplift) was the ‘middle’ housing market. Therefore, interestingly, if we applied the best percentage uplift figure (i.e. from the ‘lower’ market percentage uplift), to the ‘middle’ 1995 housing market figure, the 2017 figure of £427,344, would have been £448,387 instead – quite a difference you must agree?

Now, I have specifically not mentioned the upper reaches of the Greenwich housing market for several reasons. Firstly, the lower or middle market is where most of the buy to let investment landlords buy their property and where the majority of property transactions take place. Secondly, due to the unique and distinctive nature of Greenwich’s up-market property scene (because every property is different and they don’t tend to sell as often as the lower to middle market), it is much more difficult to calculate what changes have occurred to property prices in that part of the Greenwich property market – looking at the stats for the up-market Greenwich property market from Land Registry, only 30 properties in Greenwich (and a 1 mile radius around it) have sold for £3,000,000 or more since 1997.

So, what should every homeowner and buy to let landlord take from the information that there are many micro-property markets? Well, when you realise there isn’t just one Greenwich Property Market, but many Greenwich “micro-property markets”, you can spot trends and bag yourself some potential bargains. Even in this market, I have spotted a number of bargains over the last few months that I have shared in my Property Blog and to my landlord database, especially in the ‘lower’ and ‘lower/middle’ market. If you want to be kept informed, have a look at my blog https://greenwichpropertyblog.co.uk/ .. it’s free to do so and I’m sure you wouldn’t want to miss out – would you?

I would love to know if you have spotted any micro-property markets in Greenwich.

According to my research, of the 10,819 properties in Greenwich, 3,541 of those properties have mortgages on them. 71.1% of those mortgaged properties are made up of owner-occupiers and the rest are buy to let landlords (with a mortgage).

According to my research, of the 10,819 properties in Greenwich, 3,541 of those properties have mortgages on them. 71.1% of those mortgaged properties are made up of owner-occupiers and the rest are buy to let landlords (with a mortgage).